Illinois Providers Report Barriers to Mental Health and Addiction Coverage for Their Patients

- Acknowledgments

- National Trends on Mental Health and Addiction Parity

- Why This Survey Was Conducted and the Need for Further Investigation

- Key Survey Results

- Conclusion and Recommendations

- Citations

Acknowledgments

Thank you to the following individuals and organizations for providing valuable input and contributions to this report:

- Members of the Illinois Parity Implementation Workgroup Coalition, including NAMI-Chicago, Illinois Chapter of the American Foundation for Suicide Prevention, Depression and Bipolar Support Alliance, Thresholds, Rosecrance Health Network, Family Guidance Centers, Gateway Foundation, Sinai Health System, MADO Healthcare, Greensfelder Law, Popovits Law Group, and Childress Loucks & Plunkett

- Michael Reisman and Tim Clement, The Kennedy Forum

- Irvin Muszynski, American Psychiatric Association

- Members of the Illinois Association of Medicaid Health Plans

- Amy Watson, Jane Addams College of Social Work, University of Illinois at Chicago

- Mary Garrison, Millikin University

We deeply appreciate their time and contributions. Being listed does not in any way constitute an endorsement of this report’s findings or recommendations.

National Trends on Mental Health and Addiction Parity

Most health plans [1] are required by Illinois and federal law to cover mental health and addiction treatment on par with other types of medical conditions.[2] In other words, health plans cannot place more stringent limitations on coverage for illnesses of the brain. These requirements are broadly referred to as “parity” and are designed to reduce barriers and improve access to care for people with mental health and addiction conditions.

Despite these requirements, however, evidence from around the country suggests many patients have difficulty getting mental health and addiction treatment covered. For example, a patient survey conducted by the National Alliance on Mental Illness (NAMI) found that patients seeking coverage from private insurers for mental health services reported being denied coverage at a rate double those seeking coverage for other medical services.[3] And, data from the Connecticut Insurance Department shows that, in 2015, insurance plans there denied utilization review requests for mental health and addiction care at a rate one-third higher than they denied requests for other types of medical care.[4]

In an effort to improve access to mental health and addiction treatment, state and federal officials have been taking steps to improve parity compliance. When New York Attorney General Eric Schneiderman investigated insurers’ coverage of mental health and addiction care, he found numerous violations of New York and federal laws, reaching settlements with six insurers and returning millions of dollars to consumers.[5] In the wake of these settlements, nearly half of the mental health and addiction claims that had been rejected were overturned on appeal.[6]

In California, the state’s Department of Managed Health Care recently concluded that Kaiser Permanente continues to violate state parity laws by failing to provide adequate mental health services on a timely basis. Based on this finding, the Department of Managed Health Care has referred the case to a separate department for possible fines.[7]

Medicaid managed care organizations (MCOs) have also been the focus of recent state and federal parity efforts. In March 2016, federal regulations were expanded to apply the federal Mental Health Parity and Addiction Equity Act of 2008 (MHPAEA) to MCOs, though Illinois’ parity law by that point already covered them. This spring, Tennessee lawmakers unanimously passed legislation to increase parity compliance transparency for that state’s MCOs by requiring them to report a range of data, including denial rates, that gets to the heart of whether plan practices are in compliance.[8]

The federal government also sees a clear need to increase parity compliance. A key part of the 21st Century Cures Act, which was enacted last December with overwhelming bipartisan support to help curb the nation’s ongoing opioid epidemic, aims to strengthen enforcement of the MHPAEA. Similarly, this August, President Trump’s Commission on Combatting Drug Addiction and the Opioid Crisis highlighted plan practices that it believes inhibit access to addiction treatment. According to the Commission, patients in need of addiction treatment are “often subjected to dangerous fail-first protocols, a limited provider network, frequent prior authorization requirements, and claim denials without a transparent process.” To address these treatment barriers, the Commission called for “robust enforcement of the parity law by state and federal agencies responsible for implementing the law.”[9]

In at least tacit recognition that coverage has been too hard to obtain, insurers have begun to change their practices to remove barriers to addiction treatment coverage. Cigna, Anthem, Aetna, and UnitedHealth Group have, for example, all recently removed prior authorization policies for medication-assisted treatment.[10]

The federal government has also made funding available to help states increase access to mental health and addiction treatment. The Centers for Medicare & Medicaid Services (CMS) has awarded Illinois and a number of other states grants to increase insurers’ compliance with existing parity laws. The Illinois Department of Insurance has committed to using this money to, among other deliverables, examine consumer and provider complaints trends relating to parity.[11]

Of course, improving compliance with parity laws is not a panacea to increasing access to care. Other non-parity barriers exist, including such things as the shortage of mental health and addiction professionals nationwide, the complexity of medical coding and billing, and the inadequate integration of mental health and addiction treatment with the overall health care system.

Why This Survey Was Conducted and the Need for Further Investigation

Nearly every stakeholder recognizes the need to increase access to mental health and addiction coverage. Yet, in Illinois, specific information is lacking about the extent of barriers to coverage of mental health and addition care. Certainly, there are anecdotal reports from Illinois patients and providers, but there is a need for more information. The best data source would clearly be claims data from health plans like the above mentioned data from Connecticut insurers. Such data, however, is unfortunately not available in Illinois because the state does not require its release, and it has yet to be provided by plans. Thus, in an attempt to increase the amount of information available, Illinois providers of mental health and addiction services participated in a survey on their experiences with health plan coverage. The results, as described in the next section, suggest that the experiences of Illinois providers broadly align with what has been reported around the country.

Survey Development and Methodology

This survey of mental health and addiction providers was developed in late 2016 by a partnership of associations, community and legal experts, and The Kennedy Forum.[12] The survey was distributed by participating provider associations to their members in the last quarter of 2016 through the first quarter of 2017, and responses were collected online using Survey Monkey during the same period. Nearly 200 medical practices and organizations responded, including psychiatrists, hospitals, and community mental health and substance use disorder providers. The survey asked providers to report how frequently both Medicaid MCOs and commercial insurers denied for any reason certain types of mental health and addiction treatment—with possible responses of “never,” “rarely,” “sometimes,” “often,” “always,” or for several questions “N/A.”[13] The survey design did not require respondents to answer all questions, such as those that were not applicable to them (e.g. if the provider does not provide a particular type of service). As a

result of specific questions not being applicable to certain providers, questions presented in this issue brief have fewer responses, with no question receiving more than 100 responses.

Survey Limitations

As mentioned above, this provider survey was conducted precisely due to the lack of claims data available. Each provider response was self-reported, and providers that received the survey decided whether or not to participate. Thus, there is no guarantee that this sample of responding providers, which is significantly smaller than the population of all mental health and addiction providers in Illinois, represents all providers’ experiences. Indeed, response rates differed significantly by type of provider.[14] Another potential limitation includes the inherently subjective frequency response categories. Nonetheless, they do provide a relative scale for providers to give their perspective on how frequently coverage is denied. It is also important to note that a claim denial does not necessarily mean that coverage was not ultimately obtained. However, significant claim denials where coverage was later granted would still suggest problems likely exist that should be addressed.

Need for Further Investigation

Despite these limitations, we believe the results described below are a valuable starting point, offering a window into coverage of mental health and addiction treatment that we would not otherwise have. The results of this survey provide a foundation to aid efforts by plan administrators, providers, regulators, and enforcement authorities to identify and remove potential barriers to treatment, which could include anything from administrative problems in medical coding to plan practices that are more stringently applied to mental health and addiction care than to other types of care. This survey may be particularly useful in highlighting transition issues relating to Illinois’ ongoing expansion of its Medicaid managed care program. In the course of only a few years and in the midst of turmoil caused by the state’s budget crisis, Illinois has moved more than 1.8 million Illinoisans into Medicaid MCOs. Based on this survey, we urge stakeholders to gather additional data and dig deeper to uncover barriers impeding access to mental health and addiction coverage. The ultimate goal of all stakeholders should be to achieve seamless coverage of care for people living with mental health and addiction challenges. Doing so would not only lead to people leading more fulfilling, healthier lives, but also promises significant cost reductions for health plans and society at large.

Key Survey Results

Frequent Denials for Mental Health and Addiction Treatment

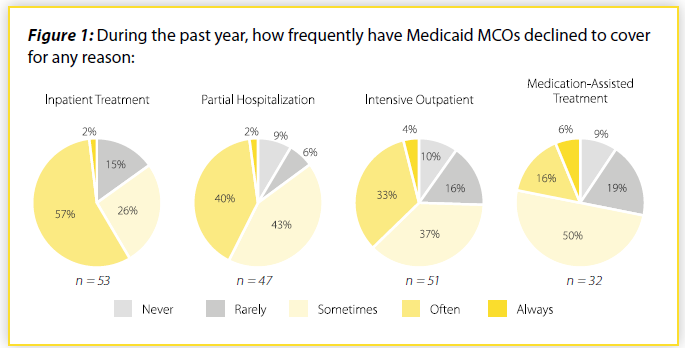

When asked about their experiences with coverage of different levels of mental health and addiction treatment that they believed were clinically necessary, responding providers reported that coverage was often denied. As Figure 1 shows, upwards of 75% of responding providers for which the question was applicable reported that Medicaid MCOs sometimes/often/always denied coverage for inpatient treatment, partial hospitalization, intensive outpatient treatment, and medication-assisted treatment.[15] The results are particularly stark for inpatient mental health and addiction treatment, where nearly 60% of responding providers reported that MCOs often or always denied coverage.

If these denials are more frequent than denials for other types of medical services, this may indicate potential non-compliance with federal and state law. These laws require most health plans that cover mental health and addiction care to pay for it using standards, processes, and procedures that are applied no more stringently than for other types of care.

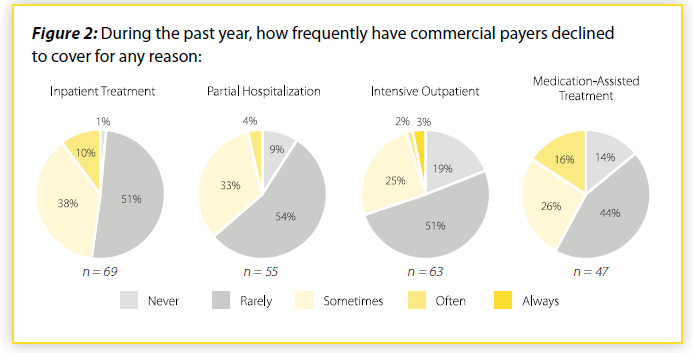

Providers also reported problems with commercial insurers (Figure 2). Nearly half of responding providers reported denial of coverage for inpatient mental health and addiction treatment occurred at least sometimes, while approximately one-third or more of responding providers reported that commercial plans at least sometimes denied coverage for partial hospitalization, intensive outpatient, and medication-assisted treatment.

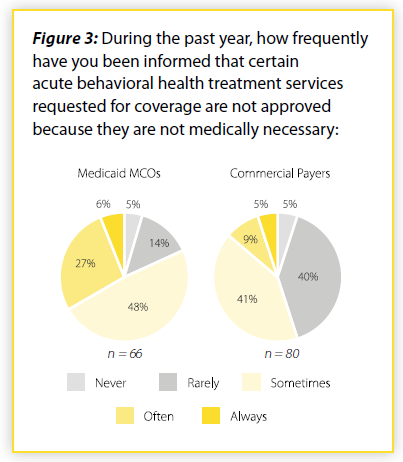

Over 80% of responding providers also reported that Medicaid MCOs sometimes/often/always deny coverage because the requested mental health and addiction treatment is considered not medically necessary (Figure 3). With commercial insurers, over half of responding providers reported the same. It is important to note that there can be valid reasons why payment for mental health or addiction care is denied. However, providers indicated that they frequently encounter barriers to payment for mental health and addiction care.

“Fail-First” and Other Barriers to Care

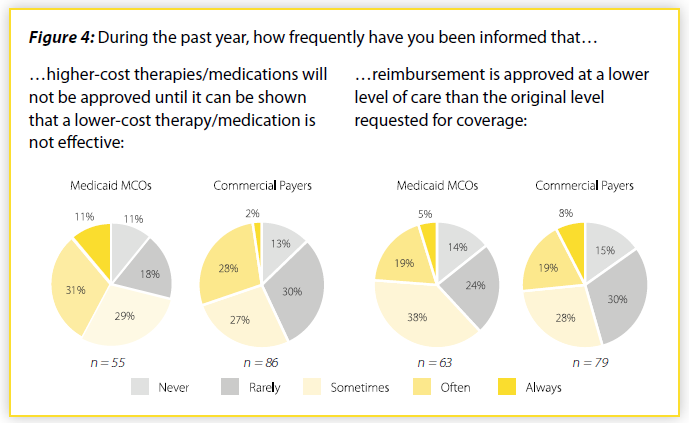

Other barriers to treatment exist beyond outright denials. For example, health plans can require that their customers “fail-first” on a lower-cost medication/treatment than the one requested by the medical professional. As shown in Figure 4, more than 7 in 10 responding providers reported that Medicaid MCOs sometimes/often/always require a patient to “fail-first.” Nearly 6 in 10 responding providers reported the same with respect to commercial plans.

Similarly, plans sometimes approve coverage for a lower level of care than the level of care the medical professional requested (e.g. a plan might only approve partial hospitalization when inpatient treatment was requested). Over 60% of responding providers reported that Medicaid MCOs sometimes/often/always approved only a lower level of care, while 54% of responding providers reported commercial insurers did the same.

Again, if health plans are more frequently requiring patients to “fail-first” or approving only lower levels of care than they do with other medical conditions, this might be inconsistent with federal and state law. Plan administrators and regulators should closely examine practices to ensure that mental health and addiction care are not subject to more stringent review. Indeed, after investigating, the New York Attorney General settled with insurers to end discriminatory “fail-first” practices.[16]

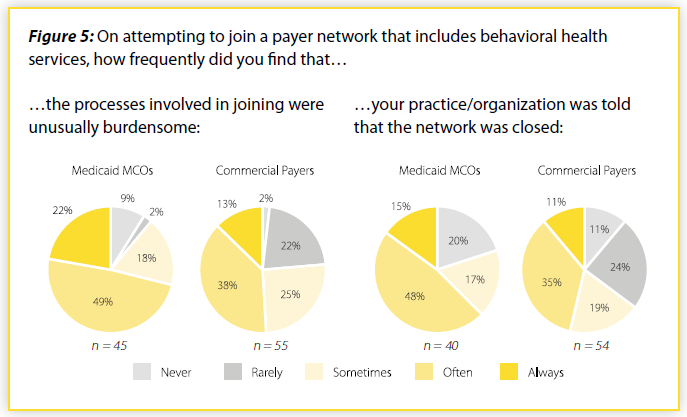

Difficulty Joining Plans’ Networks

Provider reports also support anecdotal reports of difficulty joining health plans’ networks. Nearly 9 in 10 responding providers reported that Medicaid MCO requirements for joining their networks were sometimes/often/always “unusually burdensome” (Figure 5). More than 3 in 4 responding providers reported the same about commercial insurer requirements.

Providers reported that they were also frequently told that networks were simply closed. With Medicaid MCOs, 8 in 10 responding providers reported that they were told sometimes/often/always that networks were closed (nearly 65% were often/always told this). With commercial plans, 65% of responding providers reported that they were sometimes/often/always told that networks were closed (nearly half were often/always told this).

When fewer mental health and addiction care providers are able to join plan networks, patients will have a more difficult time accessing care due to the narrow network. If plan standards and processes for admission are more stringent for mental health and addiction providers than for other types of providers, this would be inconsistent with federal and state law.

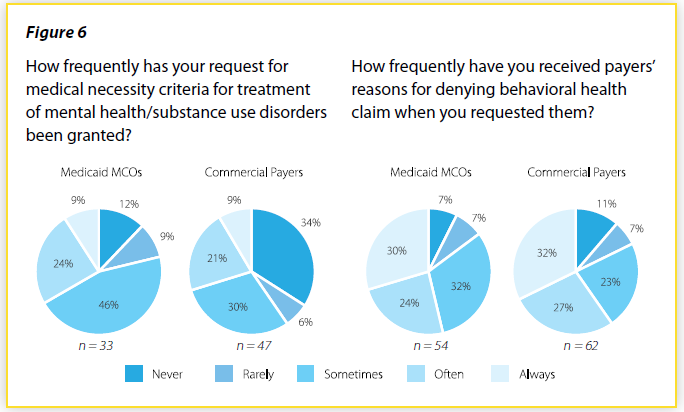

Can’t Obtain Legally Required Information

Under federal and state law, patients must receive a health plans’ medical necessity criteria and reasons for denying a claim, when requested. However, providers report that plans do not always provide this information (Figure 6). More than 9 in 10 responding providers report that both Medicaid MCOs and commercial plans have refused to provide requested medical necessity criteria. And, more than 2 in 3 responding providers report that plans have refused to provide requested reasons for denying a claim. Without these critical pieces of information, it is extraordinarily difficult for patients and providers to challenge health plans’ decisions. Plan administrators and regulators must work to ensure that this vital information is provided whenever it is requested.

Conclusion and Recommendations

The results of this survey on provider experiences suggest that problems may exist in accessing mental health and addiction coverage and that further investigation by health plans, providers, regulators, and enforcement agencies is warranted. These stakeholders should work to uncover all potential barriers to accessing mental health and addiction coverage, including plans’ compliance with state and federal parity laws, which require most plans that offer mental health and addiction coverage do so on par with other types of medical coverage. To be in compliance with these laws, plans must not apply standards, processes, and procedures to mental health and addiction care more stringently. In short, for any treatment limitation that health plans place on mental health and addiction care, a comparison must be done to ensure

that this treatment limitation is applied equally to other types of health conditions.

The following are steps that different stakeholders should take to remove coverage barriers and ensure coverage practices are consistent with state and federal law.

Health plans should conduct internal parity analyses that compare coverage standards, processes, and procedures for mental health and addiction treatment to those of other medical conditions. Plans should look at potential red flags such as higher denial rates for mental health and addiction care. These survey results also indicate that plans should evaluate their network admission procedures, as well as ensure that medical necessity criteria and denial reasons are provided upon request. Finally, plans should work to identify any other type of barriers that exist to coverage of mental health and addiction treatment.

Public regulators should regularly review plan data, particularly with respect to denial rates of mental health and addiction care. It is critical that regulators ask about and compare the standards, processes, and procedures that plans use for mental health and addiction care and other types of medical conditions. This comparison is essential to establishing whether plans are in compliance with parity laws and should occur on a regular basis and whenever periodic market conduct examinations occur.

In Illinois, the Department of Healthcare and Family Services (IHFS) has regulatory authority over Medicaid MCOs, while the Department of Insurance (IDOI) has authority over many commercial plans. As part of the recent re-bid of the state’s Medicaid MCO contracts, IHFS should include reporting language like Tennessee’s directly in the new state contracts. At minimum, IHFS should ask MCOs to report on this information annually. IDOI should thoroughly review insurance plans’ compliance with parity laws prior to state certification, as well as review plans’ actual processing of claims through regular market conduct examinations. Finally, both IHFS and IDOI need to work closely with health plans to provide the necessary guidance in writing to assist plans in their compliance with state and federal law. MCOs, in particular, have indicated that receiving written guidance prior to regulatory changes would help them better anticipate problems and make ongoing transitions smoother.

State legislators should enact legislation that increases transparency by requiring health plans to report data and information necessary to determine whether plans are in compliance with parity laws.[17] Legislators also have a critical role to play in overseeing the work of regulators. Members of the General Assembly should ask questions to ensure that Executive Branch agencies are fulfilling their responsibilities under state law.

Providers should work with health plans to identify any administrative problems (e.g. coding issues) that might result in denials. Providers are also in a unique position to help inform patients of their rights and, when an adverse determination occurs, direct patients and their families to resources to help them appeal and potentially file complaints.

Consumers can aid compliance and protect their rights by 1) requesting information such as medical necessity criteria and reasons for any denials and 2) filing appeals with their plans and complaints with the Illinois Attorney General’s Office and the appropriate regulatory agency.[18]Together, stakeholders can increase access to mental health and addiction treatment. Doing so will not only improve the well-being of people living with mental health and addiction challenges but will also reduce other health care and social costs. With strong laws in place on mental health and addiction parity, it is incumbent upon stakeholders to ensure that the promise of these laws is a reality.

Citations

[1] Parity laws apply to all Medicaid managed care organization plans and to nearly all commercial insurance plans. However, these laws do not apply to Medicare.

[2] Frequently referred to as medical/surgical.

[3] NAMI, A Long Road Ahead: Achieving True Parity in Mental Health and Substance Use Care, 2015, https://www.nami.org/About-NAMI/Publications-Reports/Public-Policy-Reports/A-Long-Road-Ahead/2015-ALongRoadAhead.pdf.

[4] Calculations based on utilization review data from the Connecticut Insurance Department’s Consumer Report Card on Health Insurance Carriers in Connecticut, October 2016, http://www.ct.gov/cid/lib/cid/2016_Consumer_Report_Card_on_CT_Health_Insurance_Carriers.pdf.

[5] Legal Action Center, “New York Attorney General Parity Enforcement,” https://lac.org/resources/substance-use-resources/parity-health-care-access-resources/new-york-attorney-general-parity-enforcement/.

[6] Michael Ollove, The Pew Charitable Trusts, “Despite Laws, Mental Health Still Getting Short Shrift,” May 7, 2015, http://www.pewtrusts.org/en/research-and-analysis/blogs/stateline/2015/5/07/despite-laws-mental-health-still-getting-short-shrift.

[7] Jenney Gold, Kaiser Health News, “Kaiser Permanente Cited—Again—For Mental Health Access Problems,” June 30, 2017, http://khn.org/news/kaiser-permanente-cited-again-for-mental-health-access-problems/.

[8] Tennessee General Assembly, Senate Bill 837, http://wapp.capitol.tn.gov/apps/BillInfo/Default.aspx?BillNumber=SB0837.

[9] Interim report of the President’s Commission on Combatting Drug Addiction and the Opioid Crisis, August 2017, https://www.whitehouse.gov/sites/whitehouse.gov/files/ondcp/commission-interim-report.pdf.

[10] Shelby Livingston, “Access Denied: Insurers slowly removing barriers to addiction treatment,” Modern Healthcare, April 14, 2017, http://www.modernhealthcare.com/special/opioid-addiction.

[11] Centers for Medicare & Medicaid Services, Illinois Health Insurance and Consumer Protection Grant Award Notice, October 31, 2016, https://www.cms.gov/CCIIO/Programs-and-Initiatives/Health-Insurance-Market-Reforms/il-cpg.html

[12] Participating associations were the Illinois Association for Behavioral Health, the Community Behavioral Healthcare Association of Illinois, IARF, the Illinois Psychiatric Society, and the Illinois Health and Hospital Association. Staff of Health and Medicine Policy Research Group also assisted with the survey design. Participants in a coalition to advance mental health and addiction parity in Illinois provided valuable feedback.

[13] “N/A” responses are excluded from the denominator in the charts in this brief

[14] A total of 1,331 providers received the survey, and 193 responded—a response rate of 15%. Of the 211 hospitals receiving the survey, 123 responded—a response rate of 58%. Of the 950 psychiatrists who received the survey, 43 responded—a response rate of 5%. Of community mental health and substance use disorder providers, 170 responded—a response rate of 16%. Because minor overlap exists in the membership of three community mental health and substance use disorder associations, the number of providers receiving the survey (170) includes a small number of duplicates (organizations receiving the survey link from more than one association). Not counting any duplicates, this number would be slightly lower, and the response rate slightly higher

[15] In general, partial hospitalization is a higher level of care than intensive outpatient treatment (e.g. more frequent and longer treatment sessions, as well as more comprehensive supports). Intensive outpatient treatment can often be a step-down from partial hospitalization. Medication-assisted treatment is a specific type of treatment for substance use disorders that combines medications and behavioral therapy

[16] The Pew Charitable Trusts, “Despite Laws, Mental Health Still Getting Short Shrift.”

[17] For example, Illinois General Assembly, 100th General Assembly, House Bill 68, Amendment 1, http://www.ilga.gov/legislation/100/HB/PDF/10000HB0068ham001.pdf.

[18] Consumers can call the Attorney General’s Health Care Helpline at 1-877-305-5145. They can reach the Illinois Department of Insurance Office of Consumer Health Insurance at 1-877-527-9431 or at

http://insurance.illinois.gov/OCHI/office_consumer_health_ins.asp. For Medicaid MCOs, consumers can visit https://www.illinois.gov/hfs/MedicalProviders/cc/Pages/ManagedCareComplaints.aspx. For appeal resources and to register a complaint that will help shape public policy, consumers can also visit www.parityregistry.org.